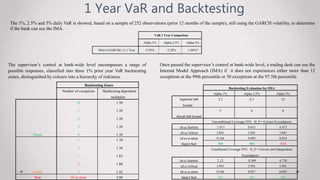

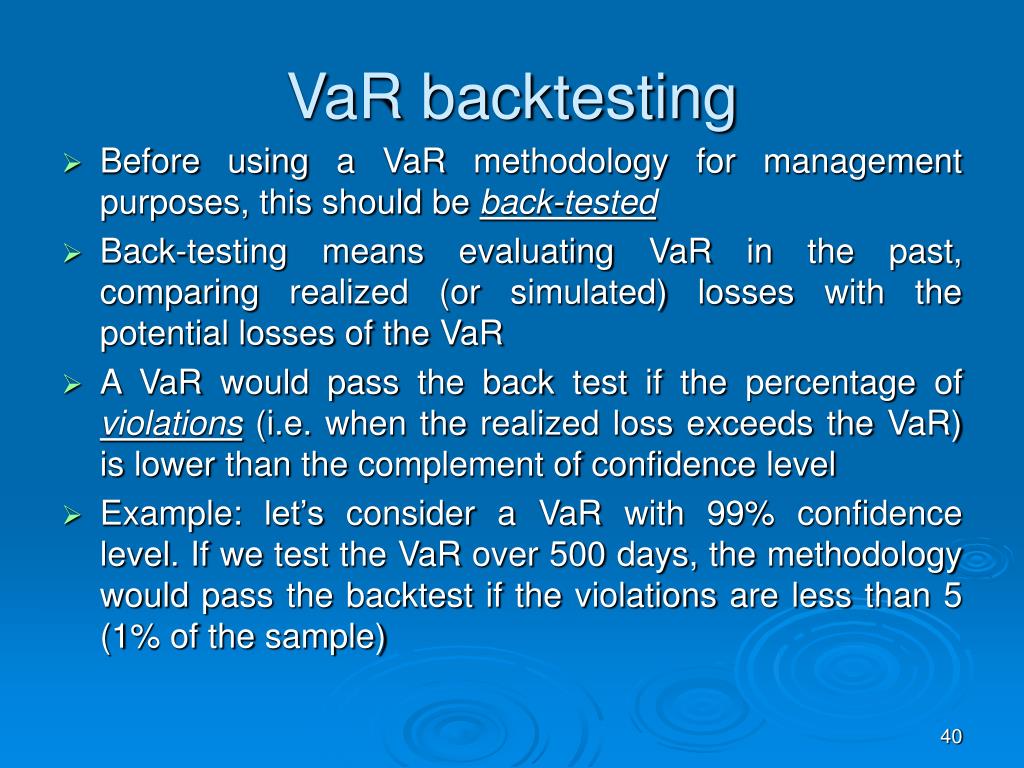

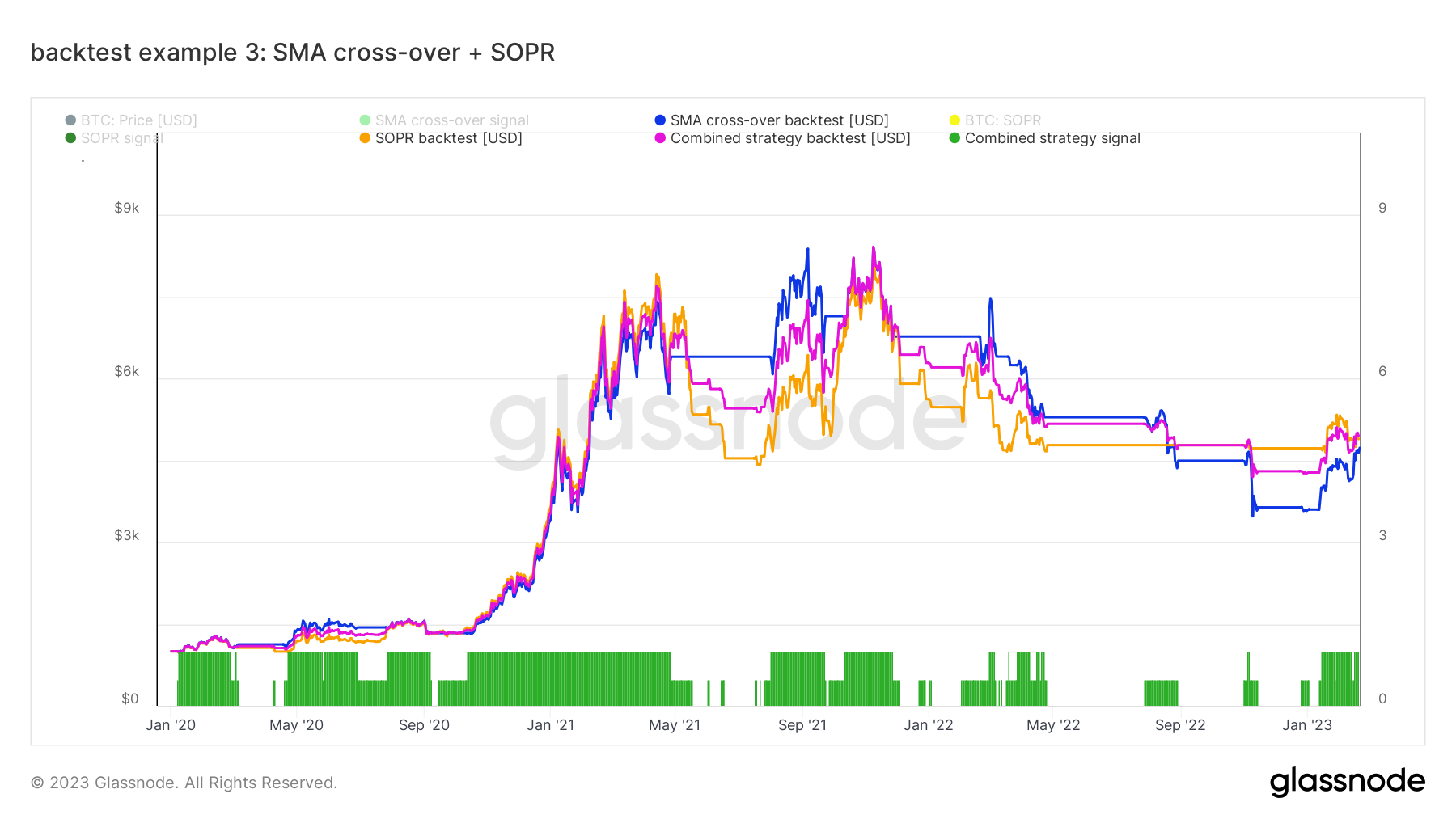

Showing 119 of 119on this page. Filters & sort apply to loaded results; URL updates for sharing.119 of 119 on this page

Power of a VaR BackTest (FRM Part 2, Book 1, Market Risk, Backtesting ...

VaR backtest test results and coefficients of variation for each model ...

Backtest results of riskmetrics VaR in the normal and full periods ...

1% VaR forecast backtest results. | Download Table

FRM: VaR model backtest - YouTube

Saddlepoint backtest of tail risk of VaR Saddlepoint backtest of tail ...

5% VaR forecast backtest results for 2018. | Download Table

Solved A backtest of 1% VaR with 100 observations yields 20 | Chegg.com

Review of Backtest For Var | PDF | Value At Risk | Estimator

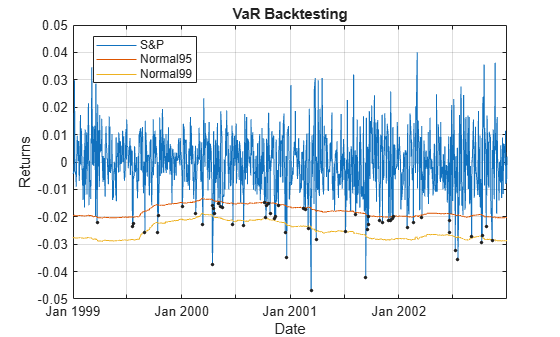

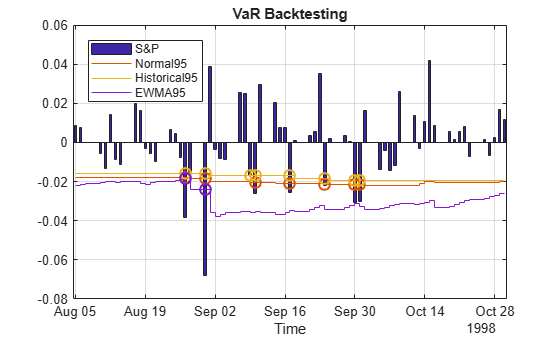

VaR Backtesting Workflow - MATLAB & Simulink

6: Combined figure of the VaR backtesting with different fat-tailed ...

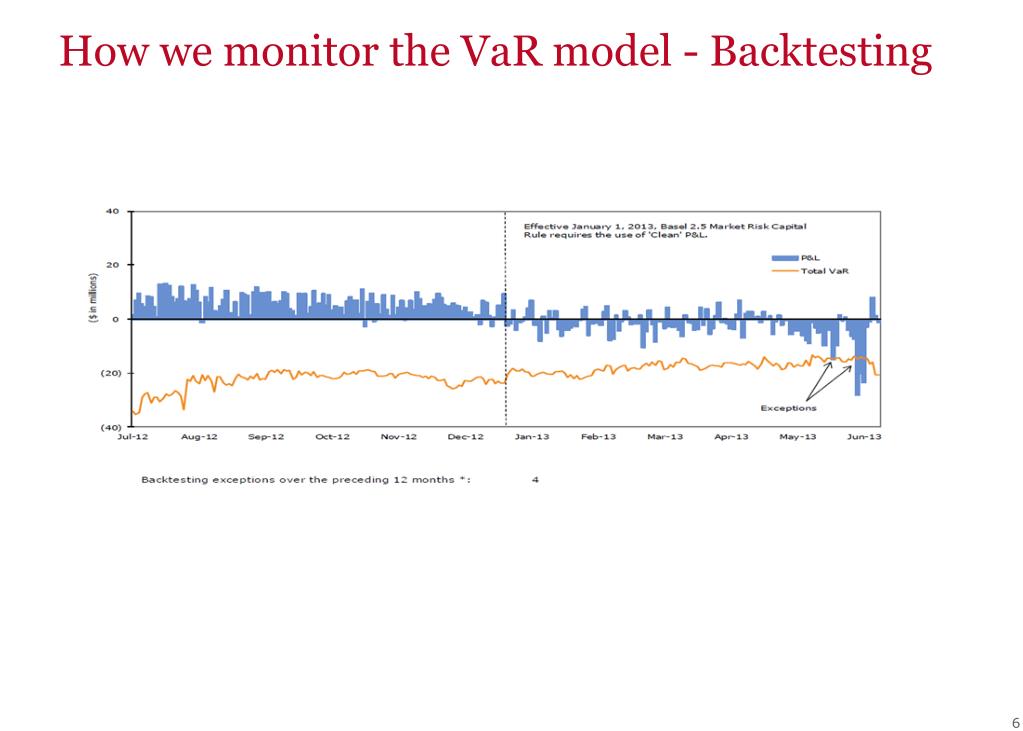

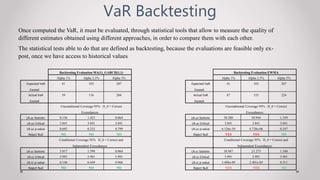

Backtesting var | PPTX

Estimate VaR for Equity Portfolio Using Parametric Methods - MATLAB ...

VaR and ES for Whole Sample Period | Download Scientific Diagram

VaR Backtesting Calculator Excel Template - Free Download

BackTesting VaR - FRM Part 2 - MidhaFin(MF)

VaR Backtest: UC, CC, and DQ tests | Download Scientific Diagram

Backtesting VAR Explained Simply - YouTube

Backtesting VaR estimation under normal distribution. | Download ...

VaR Backtesting in Turbulent Market Conditions : Enhancing the ...

VaR Backtesting | PDF | Intervalo de confianza | Errores tipo I y tipo Ii

Monte Carlo-Based VaR Estimation and Backtesting Under Basel III | MDPI

VaR Backtesting for gold return | Download Scientific Diagram

IMAT VaR backtest, from 2014-02-05 to 2017-06-07. | Download Scientific ...

Backtesting VaR and Kupiec Test Methods

"Mastering VaR Backtesting: A Practical Guide to Model Validation with ...

Proportion of VaR estimations classified as 'Green', 'Amber' and 'Red ...

VaR backtesting statistics at 95% confidence interval | Download ...

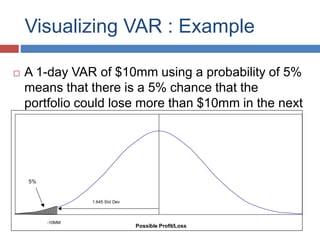

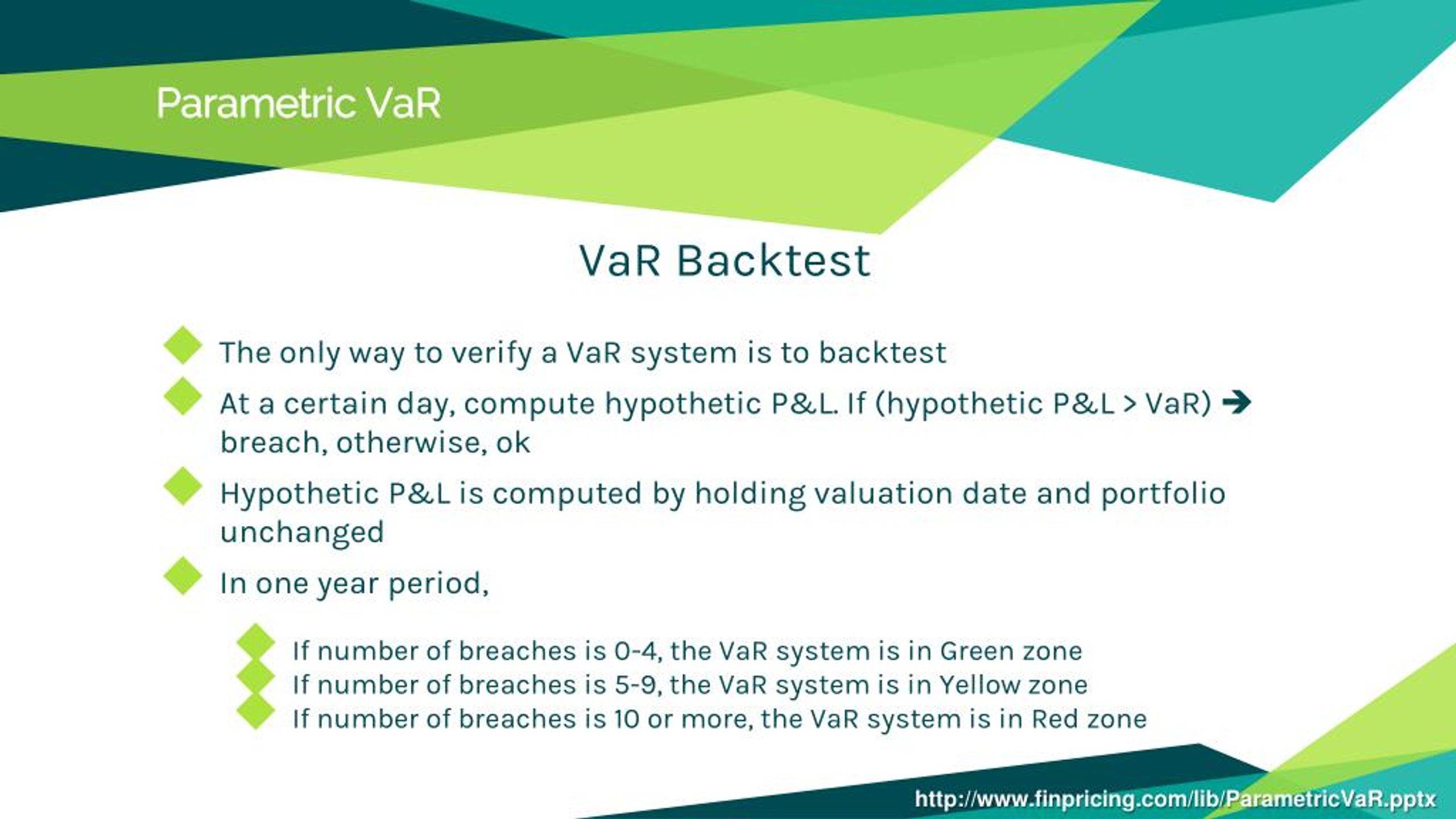

PPT - VaR Introduction I: Parametric VaR PowerPoint Presentation, free ...

IEEX VaR backtest, from 2014-02-05 to 2017-06-07. | Download Scientific ...

Backtesting Results of VaR and ES with Interest Rate Exposure ...

IBOV VaR backtest, from 2014-02-05 to 2017-06-07. | Download Scientific ...

Value at Risk (VaR) Backtest (FRM T5-04) - YouTube

21): Backtesting VaR graph for EVT-GARCH (full line), EVT (dashed line ...

VaR forecasts of portfolio risk for one day along with backtesting and ...

The Results of VaR Backtesting | Download Table

GitHub - riskarcane/var-calculator: Comprehensive VaR calculator with ...

VaR Backtesting Masterclass - Basel Regulation & Model Validation - YouTube

Value at Risk VaR Backtesting Evidence F | PDF | Value At Risk | Risk

INDX VaR backtest, from 2014-02-05 to 2017-06-07 | Download Scientific ...

Backtesting VaR - Learnsignal

VaR Backtesting Results for ARMA(1,1)-GARCH(1,1) with Student's t and ...

Backtesting VaR estimation under GARCH-EVT model. | Download Scientific ...

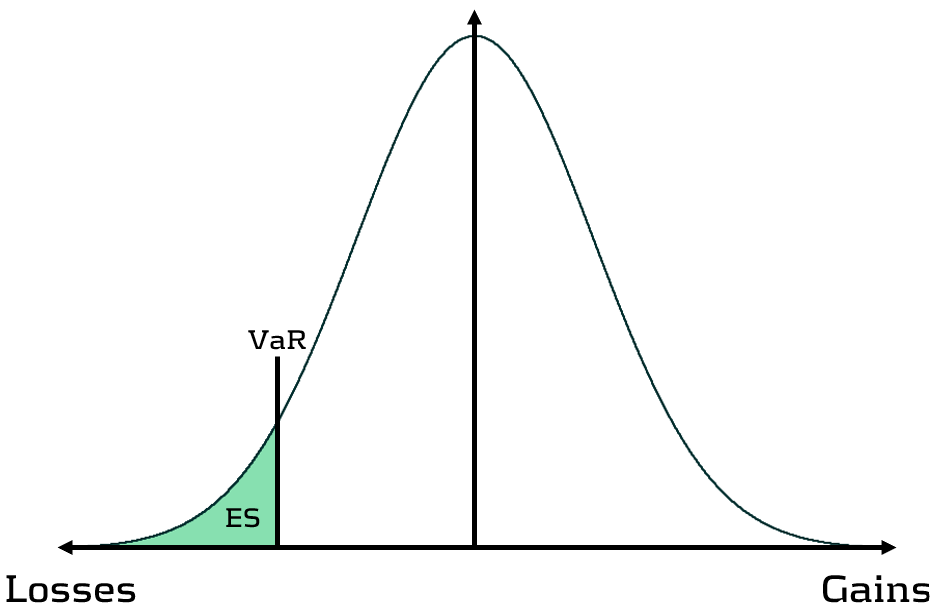

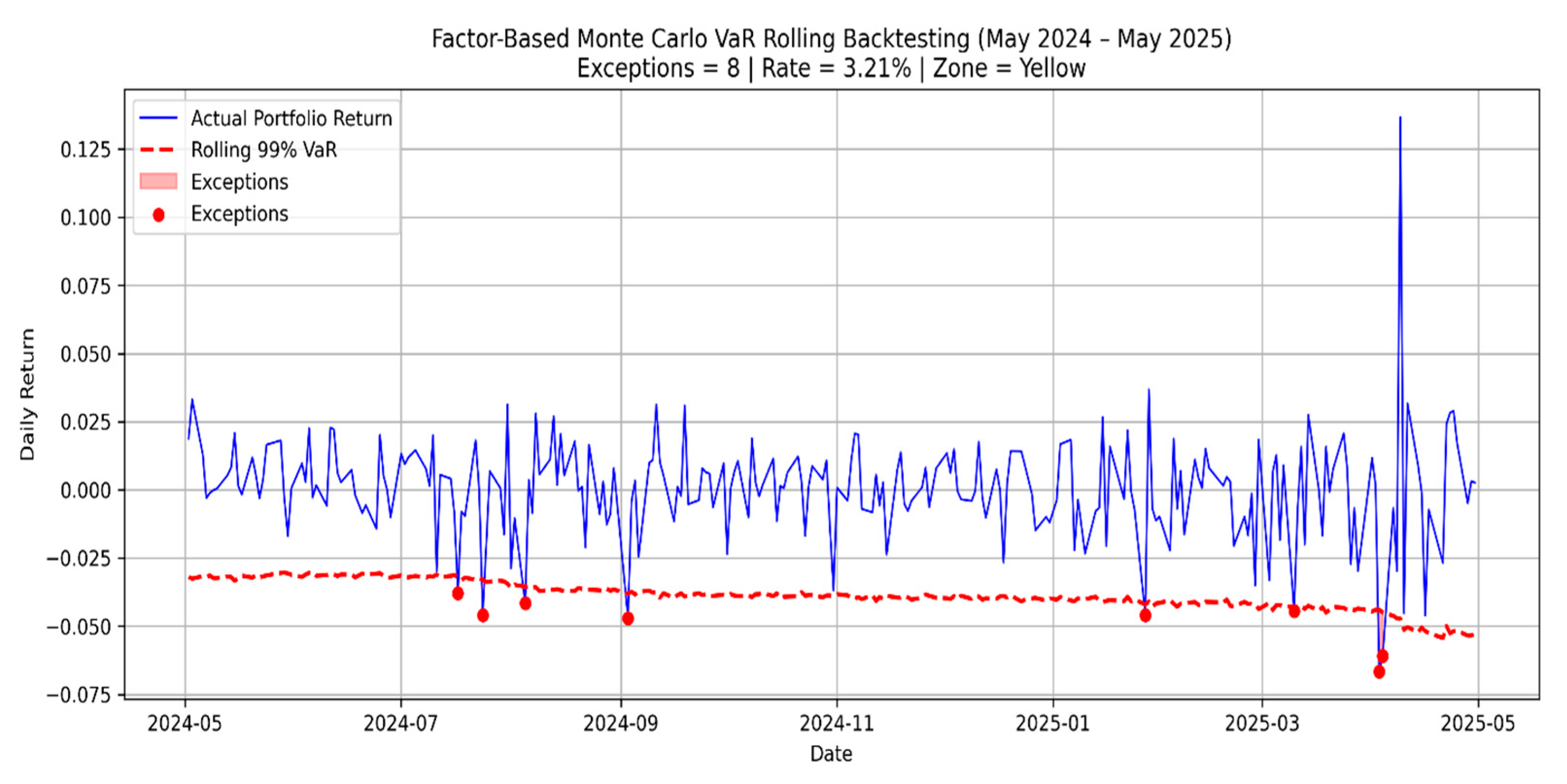

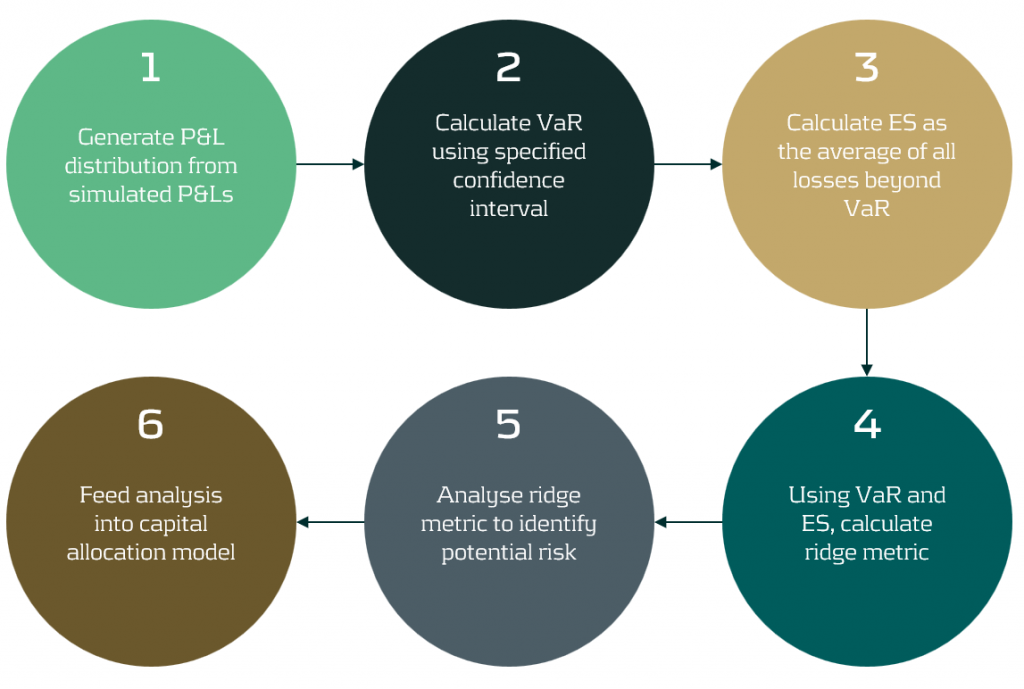

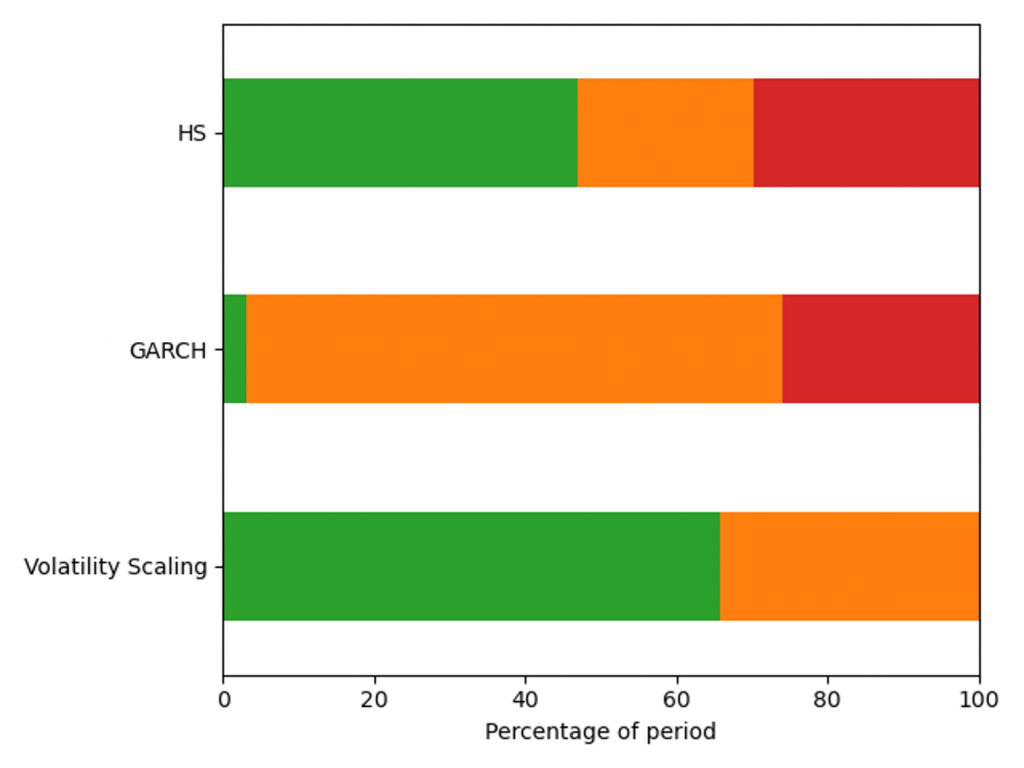

The Ridge Backtest Metric: Backtesting Expected Shortfall - Zanders

Monte Carlo-Based VaR Estimation and Backtesting Under Basel III

Backtesting VaR estimation under stable distribution. | Download ...

VaR backtesting: rejection frequencies. | Download Table

Backtesting 95% VaR Estimation of All Models (with bonds) | Download ...

Overview of VaR Backtesting - MATLAB & Simulink

Number and percentage of VaR violations derived from seven different ...

Backtesting VaR Thresholds | Download Table

Backtesting VaR analysis for benchmark models. Volume weighted market ...

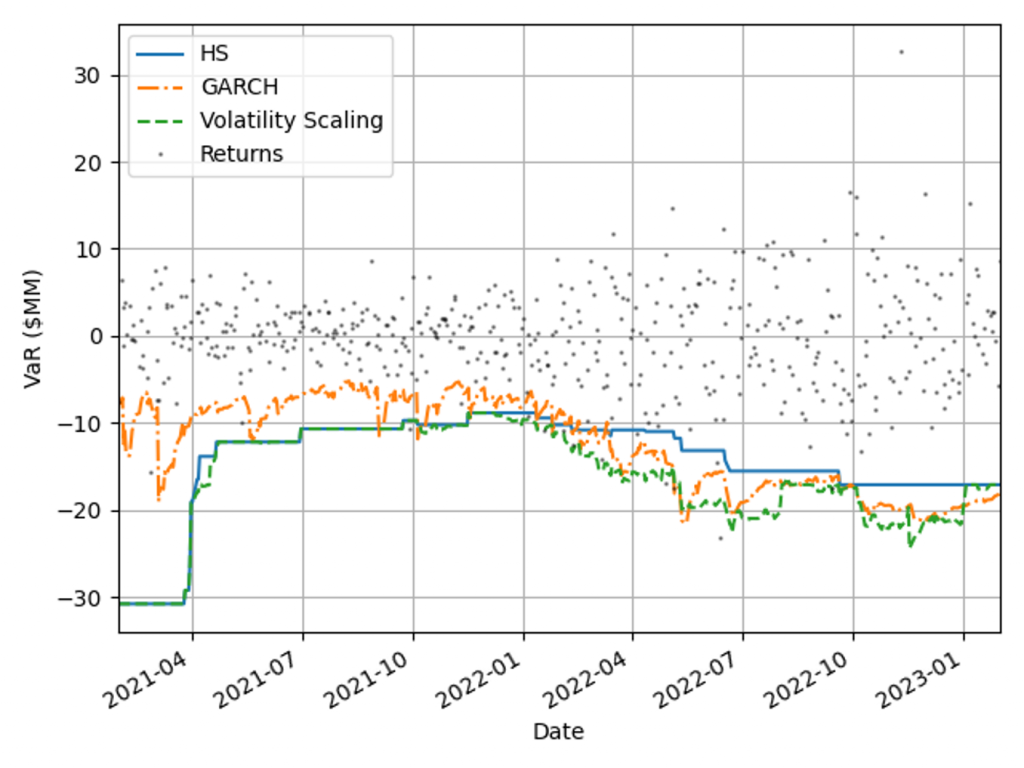

Backtests of 10-day VaR based on optimal variance forecast | Download Table

MR 4. Backtesting VaR

Backtesting VaR (Value at Risk) - YouTube

Backtesting of VaR forecasts at 95% confidence level. | Download ...

Backtesting VaR in R. VaR models are only useful if they can… | by Kyle ...

Evaluating VaR Backtesting: Techniques and Analysis | Course Hero

FRM Part 2: MR 4. Backtesting VaR - YouTube

VaR backtesting results based on 5% quantile level. | Download ...

Backtesting VaR Thresholds for One-Step-Ahead Forecasts. | Download Table

P2.T5. Lecture 3: Backtesting VaR Models and Error Analysis - Studocu

FRM Part2 Notes: VaR BackTesting

PPT - Practical Problems with Building Fixed-Income VAR Models ...

VirtualOil portfolio benchmarking and VaR backtesting - SAS Voices

Lezione 6 - Backtesting Va R - Backtesting VaR Models Andrea Sironi MSc ...

backup: Using SAS/IML for high performance VaR backtesting

Schematic diagram of VaR and logarithmic returns calculated using ...

[WEBINAR] Metodologías de VAR y Backtesting para aseguradoras - Activa ...

backtesting-var-model-exceedances - CFA, FRM, and Actuarial Exams Study ...

Value-at-Risk Estimation and Backtesting - MATLAB & Simulink Example

plot - Visualize value-at-risk (VaR) or expected shortfall (ES) and ...

EDGAR Filing Documents for 0000750556-15-000065

PPT - Value at Risk: Market Risk Models PowerPoint Presentation, free ...

Presentazione tesi | PPT

Backtesting

Sequential quantile estimation (VaR backtest) of a long position in ...

PPT - Class 2 Measuring Market Risk PowerPoint Presentation, free ...

Backtesting - MATLAB & Simulink

VaR-Backtesting/input/quantile_predicitons.txt at master · BayerSe/VaR ...

Grade comparison—VaR backtesting. | Download Table

Valuation Backtesting at Eugene Julian blog

PPT - Applied Business Statistics Case studies Market risk management ...

Backtesting Value-at-Risk (VaR). Value at Risk (VaR) is used to model ...

Forecasting the Impact of Information Security Breaches on Stock Market ...

Figure 1 from Backtesting Value-at-Risk Models | Semantic Scholar

Backtesting Value at Risk (VaR) | Finance Train

An Analysis of Different Methods for Backtesting Value at Risk (VaR ...

Backtesting historical VaR: out of sample testing - YouTube

Figure 1 from The geometric-VaR backtesting method | Semantic Scholar

GitHub - felipeOL10/VaR-CVaR-and-VaR-backtesting

VirtualOil Portfolio benchmarking and forward month analysis - SAS Voices

Oil benchmark back in the money, for now, with an eye on volatility ...